Vol. 35, No. 04

February 18, 2019

Trump and the Federal Reserve

With President Trump being the first U.S. president in decades to be even nominally against the Federal Reserve and the problems it causes, it’s time for a Fed refresher. ...

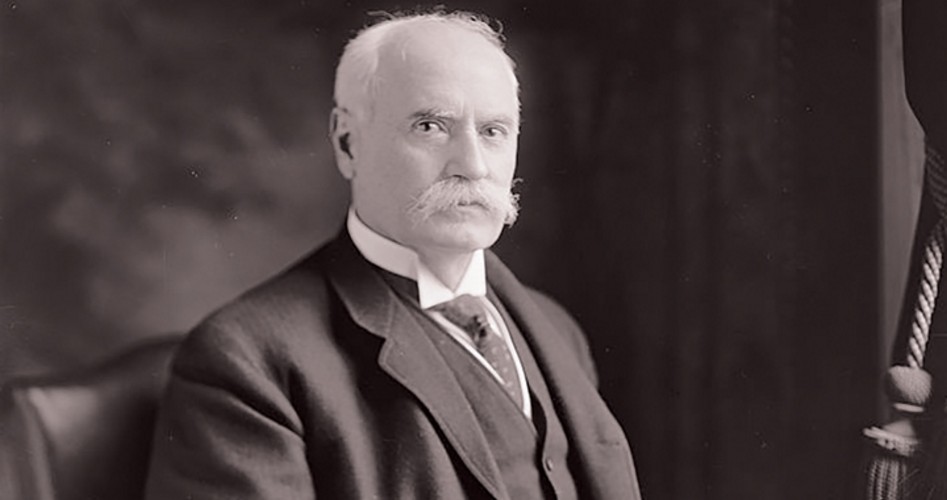

In December 1965, Federal Reserve Chairman William McChesney Martin was summoned to the ranch of President Lyndon Johnson for a dressing-down. President Johnson, a believer in the fiscal stimulus programs enacted by his predecessor, John F. Kennedy, wanted to cut taxes further, and expected the Fed to do its part by keeping interest rates low. Martin, however, was of the opinion that interest rates should be raised, arousing the ire of the volatile president.

Ushered into what he expected would be a calm meeting with the president, Martin was shocked to find himself being physically shoved around the living room and against the wall by a furious Lyndon Johnson, who kept screaming at him, “Boys are dying in Vietnam, and Bill Martin doesn’t care!” President Johnson had apparently never gotten the memo on the supposed independence of the Federal Reserve from political influences. Cowed by the president’s belligerence, the Fed chairman maintained interest rates very low that year and the next, putting the lie to the Fed’s alleged detachment from tawdry politics.

In our time, we again have, in Donald Trump, a president openly hostile to the Fed and its policies. Trump, be it noted, has shown no inclination to physically assault Fed chairmen. But his withering anti-Fed rhetoric on Twitter has shocked the sensibilities of the East Coast establishment because, in the years since Johnson’s outburst, criticism of the Fed simply hasn’t been acceptable to the Powers That Be. Throughout its history, the Federal Reserve has maintained a public posture of independent decision making and immunity to criticism. But the reality behind the scenes is a central bank beholden to special interests both public and private, determined to maintain the traditional veil of secrecy and special privileges that have always concealed its true nature from the general public.

Premium Content

Sign in with your ShopJBS.org account to read the full article, or subscribe below for unlimited digital access.

Log In to Continue Reading

- 12 Issues Per Year

- Digital Edition Access

- Digital Insider Report

- Exclusive Subscriber Content

- Audio provided for all articles

- Unlimited access to past issues

- Cancel anytime

- Renews automatically

- 12 Issues Per Year

- Print edition delivery (USA) *Available Outside USA

- Digital Edition Access

- Digital Insider Report

- Exclusive Subscriber Content

- Audio provided for all articles

- Unlimited access to past issues

- Cancel anytime

- Renews automatically